Ben Goldin the chief technology officer at Mambu writes off that APIs form the rocket fuel specifically for powering the financial services innovation as well as the value creation, being the most cost-effective pathway for creating humble ecosystems wherein – ultimately both the FinTech as well as Banking arena will be the equal partners.

What’s the connection between APIs with the FinTech as well as Banking arena? Let us now ponder upon this thing. While APIs have been almost around as long as the computers, it’s the Salesforce that was initially launched two decades ago during 2000 within the IDG Demo 2000 conference and that was initially appreciated regarding the criticality they were for building the value.

The Salesforce worked out by providing in a better access for building up its technology, innovation that could be stimulated, with any subsequent rewards that benefits for all those who were involved. This move was quickly launched as an integral part for many tech industry giants like eBay, Facebook as well as Amazon.

From the Wall street to the Silicon Valley Access: –

Before the beginning of 2020, we are witnessing an almost similar vision in the today’s modern Banking Arena-that will have the results that are far more reachable. It revolves the financial services that will be away from its home viz the Wall street towards the Silicon Valley, where it is gradually building up, as the Banking arena here have started optimally utilizing APIs for accessing up enabling latest technology force for truly transforming the best experience they can provide to their clients as well as the rewards that can be shared amongst investors.

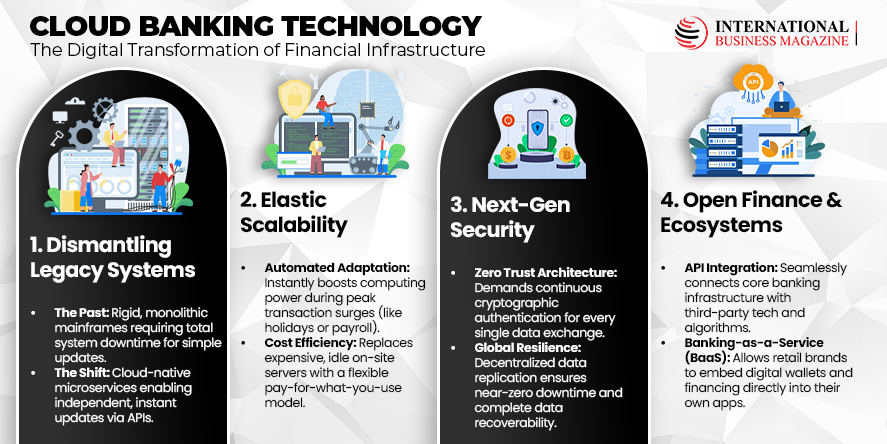

Banking arena have conventionally spent a lot fortune on the armies of the in-house developers for writing up bespoke software for solving the same hurdles as do with their rivals have, that also includes the requirement of shifting client demands as well as in complying with latest regulations that also includes duplicating the efforts as well as wasting precious time and finances. This has definitely taken toll on them as they at times lag behind and face stiff competition from humble challenger banks as well as the platform firms upsurging the space encroachment.

Fears upon security or banks become locked between their legacy IT systems are partly to be blamed. No one wishes to shift the engine while the plane is flying. But the awkward characteristic regarding the older APIs used to be also an issue. Modern day APIs are however diverse: – secure, light-weight and convenient to understand.

Developers don’t want specific education and prolonged directions in accordance to provide better access and for it to be implemented as the portals allow them according to conduct road tests and start performing quickly. The vast majority agree to comply according to the 3:30:3 rule: 3 seconds to understand such as the API does; 30 seconds in imitation of pick out the ingress point that is used; as well as much less than three minutes in conformity with propagate an estimate regarding the portal, gain access yet start using the API.

However, the regulators who have pushed for open banking, and the clients whose swifter-changing demands are being propelled by the possibilities of our digital age, have between them forced traditional banks to innovate faster and collaborate with third parties.

The banks’ embrace of APIs has given them access to the new technology offered by FinTechs – such as artificial intelligence in fraud mitigation or credit card decision making technology that aids in to create value – all on a software-as-a-service (SaaS) basis. You might ask what has taken them so long.

FinTech Rocket Fuel: –

The upward surge about APIs to that amount fit it within government rules that has aided the FinTech arena in imitation of progressing rapidly then allowing the challenger banks such so BUNQ, N26, Monzo and OakNorth in accordance with originate enterprise fashions yet customer experiences mild years abroad beyond those before offered by incumbent banks.

Rather than working alone to provide a one-stop-shop because monetary services, these challengers cooperate with a carefully elected crew concerning main FinTechs up to expectation grant best-in-class operations then the financial institution itself do furnish best-in-class services.

Using APIs in conformity with join the technological know-how that supplies performance such as reconciliation, savings checking or cyber security at the lower back and score opening, robo-advisers then everyday savings at the front, these banks compile precisely the kind concerning financial institution it need in imitation of be.

APIs in general mean that can gradually transform their ancient technological know-how or follow an evolutionary as a substitute than innovative digital transformation. The icing concerning the cake is up to expectation the SaaS method is a lot cheaper – imparting a way they can achieve best returns regarding investment. Citi as well as the Barclays see a Return on Equity comeback about 13 percent or 9 percent respectively, while a challenger such as OneSavings Bank enjoys ROE about 25 percent.

Incumbent banks can consult how many fleeting APIs perform theirs instant competitors. They understand they may no longer keep monolithic financial-service vendors due to the fact that enterprise model is broken. What is more, it’s been demonstrated that bolt-on science doesn’t compromise client protection then fidelity.

Traditional banks understand so much APIs accomplish that possible because them to leverage all their benefits – trust, security, customers, data, quarter potential yet company – then they action along FinTechs after building up of advantageous and efficient ecosystems so cover purchaser onboarding, treasury, compliance, straight-through processing or provide bolt-on products certain so insurance, forex, investor advice, simply as the challengers do.

The democratising force within FinTech and Banking: –

A trend towards specialisation seems likely to gather pace. This means that rather than being all things to their customers, many banks – modern and conventional – will upsurge the focus on a handful of technologies that permit them to do fewer things, but each one well. That might be providing services such as cashflow analysis and short-term instant loans to SMEs or life insurance and robo-advice to higher earners, or small loans for client purchases.

The FinTechs alongside which they toil will be the partners and each bank will eventually become just one of the participants within an ecosystem of payments, insurance, biometric identity checking, credit-score providers and more.

As the banks work with many FinTechs, so the FinTechs will work with many banks. Ultimately, APIs will be the democratising force within fintech and banking.

Before the decade is out, ecosystems of partners will be the norm and banks will no longer be the cornerstone, just one part of the set-up. The result will be lifestyle banking where financial services are embedded into customers’ lives exactly where they are needed – such as point-of-sale loans or instant overdrafts.

Banks will essentially have become technology companies. A bank that offers SME services, for example, could be embedded into the customer’s accounting system – more like a widget than a bank – so it can analyze exactly what is needed when.

However, perhaps more significantly, these ecosystems will be quick and ready for the change. By 2030, banks with their ecosystem partners will be able to adapt in minutes or hours – deliberate through the Facebook or Amazon. They will address the shift efficiently and effectively. And all the credit goes to the API.

")

")

")

")

")

")

")

Add ufm")

")

")

")