The evolution of the digitalized transformation with the equal emergence of the FinTech arena is undoubtedly creating best prospects for the tech savvy banking or finance related society, with the prospect of easing up in adoption of better digitalized payment gears.

However, the still roadblock in front of the FinTech innovations is to bridge the gap created by digital divide and bring in closer the 25 million inhabitants who are still surviving with the aid of Cash mode and not able to adopt flexibly to digitalized or online payment module.

It is undoubtedly a sure thing that how the emergence of COVID-19 Pandemic and newer strain of COVID-19 have been viewed and taken as a humungous global disruptive force to reckon with the mode in which we do live, perform our duties, eat as well as procure better.

However, the advent of the COVID-19 Pandemic has definitely changed the way we live in and forced the society to view a majority of declining trend within the currency backed tradition. Certainly, within fewer nations like UK as well as Italy, the ATM extractions have in fact diminished 60-90 percent within the primary days of the Pandemic.

Although with recovery definitely on cards even with the scare of emergence of newer yet subtle strain of COVID-19, for the nations like UK, there is still a declining trend of over 35 percent downsize observed from the previous year as the CEO for largest ATM operator within the UK stated that ATM’s or cash machines may completely vanish from our sights within the forthcoming time frame.

However, it is not just the part and parcel in case of European territory, as the story continues to this part of global territory as well, wherein as per the latest report compiled by the courtesy of the payment gateway checkout.com, it has proved a huge upsurge of 85 percent within the digitalized transactions as a 47 percent of shoppers are in pursuit to adopt to procuring online as well as in providing the payment digitally.

As although it points out to be a great news for all E-Commerce firms as well as digitized companies, it still raises a popular query out of the curiosity generated amongst its end users – of how does the public who are unbanked viz not having any bank accounts transact or do financial payments without the currency?

For an illustration: – COVID-19 Pandemic’s disruption towards currency-based transactions is not just restricted on to the client perspective; as it remains applicable to even tiny scaled businesses like (barber/native shop) or an autonomous agent (gardener/plumber) – who typically do not have the facility to take non-cash or digitalized payments. An incapability to receive digital payments also grants an unfair shortcoming to these traders, exclusively when associated to bigger industries who have the means to bargain their clients online as well as digital payment solutions.

The Cash has suddenly been viewed in wake of recent unprecedented developments of the COVID-19 Pandemic as a nasty four-letter word that the current public finds it reluctant to handle the same. The global Banking as well as the FinTech corporates have been keen in innovating and deliver perfect solutions to mounting hurdles within two core pathways: –

- By taking consideration of how the businesses can authorize better clients for performing all their payments or financial transactions digitally.

- As well as by creating or manufacturing necessary merchandize, applications that will in turn empower majority of the firms for obtaining direct access of even making or getting digital payments within an offline mode as well as moving to an online mode as and when situation demands.

More than two billion adults universally do not have an admittance to a bank account. Even within the GCC, as per an estimate around 70 percent of the adult population does not own a bank account – comprising primarily of a low-income immigrants and students.

It is thus increasingly vital to ponder each feature individually while looking for to better comprehend the part that innovation drives in overcoming cash-related hurdles.

Empowering Varied Clients or End-Users: –

It is significant to comprehend that the ‘unbanked’ in the GCC are chiefly the modest income migrants – in the UAE that number is about 70 percent of the salaried population, who earn less than Dhs5,000 a month.

For an illustration: – Pondering regard a native helper – who survives with her employer, gets free accommodation as well as food, gets paid in cash and sends 90 percent of her income back home. Similar patterns exist for individuals in building or employed in large service companies – facility cleaners, hotels etc.

In countless ways migrant workforces have the bottommost consumption footprints, which means that they have been maximum affected by many of the COVID-19 related disruptions around shifting funds.

Many low-income workforces tussled harder to direct finances back to their home nations in the form of currency since most exchange houses were locked at the height of the pandemic. Furthermore, even if they could guide currency digitally, their families could not gather or spend that cash due to extensive lockdowns.

Innovations here comprised the initiatives by banks submitting free digital accounts for these patrons, which can be unlocked with only their Emirates IDs and comprehensive FinTech merchandize that permitted these patrons to share admission to their cards with their family back home – be it in any part of the world, then be it in India, Philippines or other demographics.

The core is to provide workforces with a direction to their hard-toiled cash by offering them with full prominence on how their currency is being spent, while letting them to set regular financial limits and group restrictions on what their salary can be utilized for.

Moreover, it is about offering a robust economic solution and services that offer monetary inclusion to those that have traditionally been ignored by conventional banks.

Empowering the traders: –

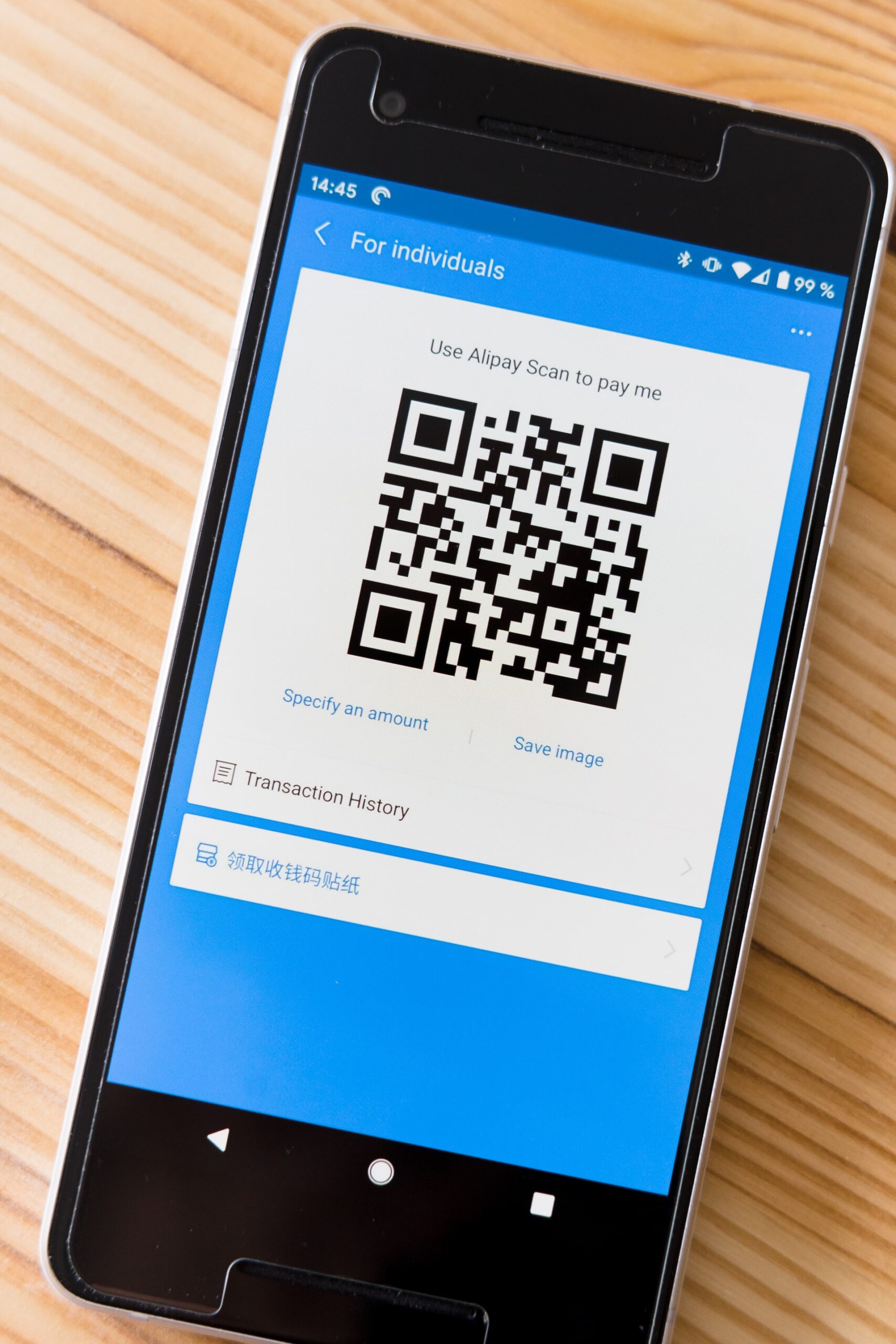

Establishments that can support offline traders digitise their expenditures or move online have been mounting in popularity across markets. In countries like India, that has a Unified Payment Interface (UPI) which empowers public to pay traders directly account-to-account utilizing the QR codes, digital expenditures have augmented rapidly. UPI payments in Oct 2020 exceeded two billion transactions, an upsurge of an 80 percent as resulted in from a year ago.

For merchants who are still not online, we have had establishments like Dukaan in India and Bukuwarung in Indonesia which have extended dramatically during the pandemic. These firms enable small traders to list their merchandize and execute online – mainly using prevailing communication tools like WhatsApp to progress the invoices and pay bills.

Even in this part of the territory, we have had initiatives like FAB’s Payit wallet which provides direct access to the traders to accept expenditures by means of the client’s Payit wallets. They have also had crucial tie up alongside the payment gateways like Telr beginning its shop tool to empower traders to speedily setup up online shop for the initial time. Even outside of small retail, we have had initiatives like Noon Food, which aided the native restaurants for admitting the online orders and distributing food.

While the world awaits a coming back to normalcy, with positive news around vaccines, it is kind to state that the pandemic has fast-tracked the long-term decline trends of currency utilization.

As societies implement more digital payment tools, it endures quite significant to take along the two billion people globally or the 25 million in the vicinity who are still alive in with the currency mode. Innovations that emphasis not only on digitisation of income (pay into account vs cash), but also on digitisation of consumption (pay digitally vs cash) will play a noteworthy role in confirming that the paybacks of digital commerce are practiced by all.

")

")

")

")

")

")

")

Add ufm")

")

")

")