Mirroring global trends, the banking sector is rapidly modernising its smart banking operations. By integrating Artificial Intelligence (AI), Deep Learning, Optical Character Recognition (OCR), and Cloud technologies, banks are transforming the customer experience through hyper-automation, AI-driven personalization, open banking, and the adoption of digital currencies by central banks across the globe. These innovations are making banking faster, seamless, and deeply integrated into everyday life.

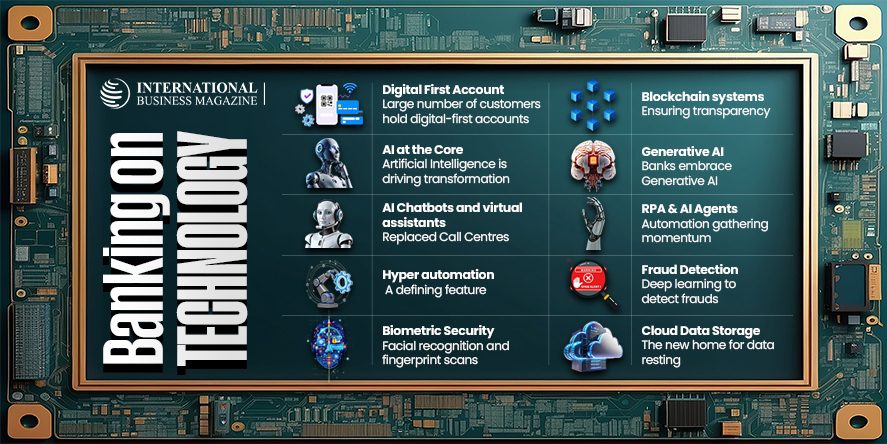

The banking trends in 2026 is a showcase of how technology can reshape finance. What began as online portals has matured into a digital ecosystem where large number of customers hold digital-first accounts. Traditional banking giants have reinvented themselves as digital-first institutions, while neobanks and other fintech challengers are pushing boundaries with lifestyle-driven platforms for tech driven finance.

The Central Banks are playing a pivotal role, introducing regulations for digital assets and launching the Digital Currencies, which ensure faster, cheaper, and more inclusive payments while reinforcing monetary credibility. Artificial Intelligence is at the heart of this transformation. Banks now deploy AI-powered personalisation, tailoring financial products to individual spending habits and life goals. Predictive analytics anticipate customer needs, from suggesting savings plans to offering real-time investment advice. AI chatbots and virtual assistants have replaced call centres, providing instant, multilingual support around the clock.

Banks were not alone in their efforts to embrace modernization and digital transformation. Customers’ expectation and demand for instant, seamless, and mobile-first banking experiences forced the financial institutions to take the leap for embracing innovative technology. In addition, the pressure to change traditional banking added to this change. At the same time, competition from fellow bankers is pushing up need for tech-driven banking.

Therefore, the banking sector took the hyper automation as a defining feature. Processes that once took days – like KYC verification, loan approvals, and compliance checks – are now completed in minutes through automated document handling and real-time analytics. This not only reduces costs but also enhances customer trust by minimising errors and delays.

For example, the UAE’s open banking, has unlocked new possibilities. Customers can securely share their financial data with third-party apps, enabling integrated experiences such as budgeting tools, investment dashboards, and lifestyle-linked rewards. This ecosystem means going beyond branches where banking is no longer confined to a branch or app – it’s embedded into daily routines, from shopping to travel. Digital wallets and biometric authentication have become mainstream. Nearly half of Gulf residents use digital wallets, and in the UAE, facial recognition and fingerprint scans are standard for secure transactions. This has created a frictionless environment where payments are instant, secure, and widely accepted.

Further, the banking system embraced real-time compliance and security monitoring to enrich the user experience. They are using Blockchain-based systems to ensure transparency in transactions, while AI continuously scans for fraud patterns. For younger, mobile-first customers, neobanks offer more than banking – they provide lifestyle ecosystems. Through gamified savings, instant bill splitting, and partnerships with e-commerce and travel platforms, these banks blur the line between finance and everyday living.

A significant tech-driven initiative in the banking ecosystem is the gradual roll out of Central Bank Digital Currency (CBDC) as part of digital banking. Just to illustrate and example in the UAE, according to Ledger Insights, following wholesale testing, the UAE Central Bank is actively progressing on the rollout of the retail version of the Digital Dirham. The UAE successfully executed live government financial transactions and the first cross-border CBDC payments with China using the multinational mBridge (and Jisr) platform recently. In 2022, India’s RBI launched Digital Rupee both for wholesale and retail customer.

Another layer of hyper automation in the banking system is the adoption of Generative AI for tech driven finance. This is transforming how the banks work. GAI has the ability to answer questions from the customers, create content, reports etc. This technology is enabling banks to provide faster and smart services with near accuracy. Banks are increasingly using Chabot supported by Robotic Process Automation (RPA) and AI agents for customer engagement as servicing customers in the competitive market condition is vital. Banks are deploying AI agents for their ability to take action on behalf of the customers such as updating accounts statements, checking balance, start, and complete loan process.

The banks are also using OCR to save time and digitise records relating to accounts, loans, and disbursements. Besides these technologies, banks are also using Deep Learning to detect frauds and embezzlements. Banks use Deep Learning to understand how customers spend, transfer money or make investments. In case of any unusual and suspect transaction, this alerts banks and the customers.

Cloud Native Infrastructure is where the banks are migrating their data and operational details. API drive banking is also part of banking tech drive to avoid having bulky in-house servers. Therefore, Cloud is the next stop for banks in terms of tech adoption. Today banking is technology driven and less human operated and moving towards touchless banking.

Conclusion

The banking sector is not only technologically advanced but also customer-centric, inclusive, and globally competitive. The story of banking in 2026 is one of speed, intelligence, and integration. Customers no longer see banking as a chore but as a seamless extension of their digital lives. From AI-driven personalisation to the Digital Currency, from hyper automation to open banking, the banking system has redefined what banking means.

Article by Imtiaz Ahmed Sharif

")

")

")

")

")

")

")

Add ufm")

")

")

")